Tax Reform Has Consequences for New York Homeowners

At the beginning of December, the U.S. Senate passed their tax bill. This followed the U.S. House passing theirs. There are differences between the two and they need to be ironed out in a conference committee.

But, it’s a good bet they will be, and that a newly polished bill will be sent to the White House for the President’s approval.

It seems inevitable.

But, ultimately it depends on several of the issues that need to get ironed out between House and Senate legislators. If homeowners don’t speak out now and convince their Members of Congress to address certain concerns, – especially those in New York – they are going to bear the brunt of this tax bill’s impact.

“We have concerns about the plan and its impact on New York state as a whole, New York taxpayers and New York homeowners – and frankly future homeowners as well,” said Mike Kelly, Government Affairs Director at the New York State Association of REALTORS® (NYSAR). “We see it as a tax break for corporations that are making record profits that are going to be paid for on the backs of New Yorkers and homeowners.”

The conference committee will be under a lot of pressure – both in time and from special interest lobbyists – to make last minute changes. And when that happens, there are always deals to be cut, usually with both sides giving in a little bit.

For example, the House bill would slash the mortgage interest deduction in half for all new mortgages, and eliminate it completely for those who own second homes. The Senate Bill would only eliminate it for home equity loans.

It sounds like there is a middle ground to be reached there, none of which will be beneficial to homeowners.

“As soon as you eliminate or reduce real estate-related tax provisions, such as the deductibility of mortgage interest or the deductibility of property taxes, there are going to be fewer people with the ability to purchase a home,” Kelly said. “This will drive demand down and when that happens, property values may decline.”

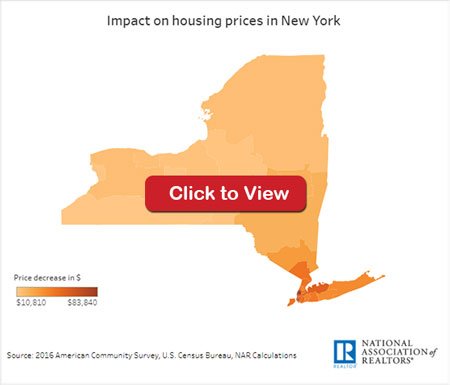

The National Association of REALTORS® (NAR) commissioned a study to see how the House bill would impact housing prices in New York state, and depending on where a home was located, values would decrease from anywhere between $10,810 and $83,840.

“New York State has higher-cost housing stock than in most places in the country,” Kelly said. “For example, the average sales price for a home in New York City (cooperatives, condos and one to three family dwellings) in the first quarter of 2017 was over $1 million – and that’s often for a first-time purchase. This is not a three-bedroom condo or co-op on the Upper West Side looking at Central Park. This is often the starting point for a first-time buyer in New York City.”

It appears that the House and Senate are ready to come to an agreement on tax reform before the end of the year.

After House Republicans warned that a Senate bid to end a long-standing deduction for state and local taxes (SALT) was a nonstarter, the Senate adopted the House plan to put a limit on that tax break to $10,000 in property taxes.

“Any reduction in the ability to deduct state and local taxes, including property taxes, will negatively impact many New Yorkers’ net income.” Kelly said. “The result for many New Yorkers will be an increase in their taxes, which will reduce their income and their ability to purchase a home.

Also, we are a high tax state and in many parts of New York State, property taxes far exceed $10,000 for what is a middle-class home.”

“Housing is a primary economic driver and anything that affects that has the potential to hurt the overall economy,” Kelly said.

Time to Focus on Affordable Housing

Taxes on real estate are not the answer. Sign the petition calling on Congress to address our country’s housing shortage.

MORE STORIES